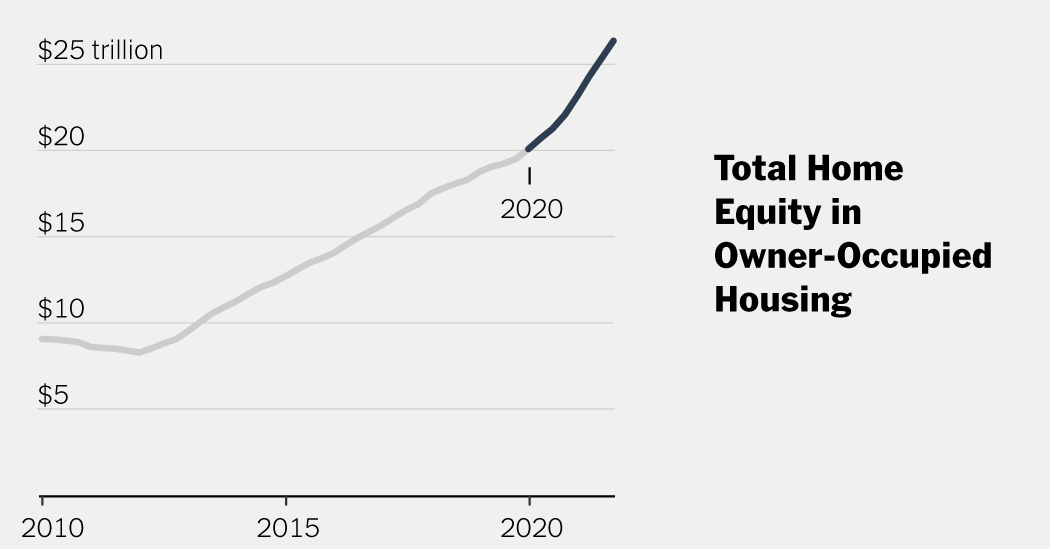

In the past two years, Americans who own their homes have acquired more than $6 trillion in home equity. To be clear, that doesn’t mean homebuilders have transferred $6 trillion worth of new homes to buyers, or existing homeowners made $6 trillion in kitchen and bathroom upgrades.

Rather, most of this money has been created by the simple fact that homes, with supply shortages and high demand across America, have soared at a record pace during the pandemic. Millions of people — widespread across the 65 percent of U.S. households who own their homes — got a share of this windfall.

It’s a remarkably positive story for Americans who own a home; it is also inextricably linked to the housing crisis for those who do not. For them, the rents add up quickly. Inflation is shrinking their income. And the very thing that created all this wealth has pushed home ownership as a means of building wealth further out of reach.

That dual reality follows what was a massive wealth creation event with few precedents in American history.

“I’m really struggling to find a parallel to this,” said Benjamin Keys, a professor at the Wharton School of Business, trying to identify a moment when so many people acquired so much wealth in such a short period of time.

In percentage terms, the stock market has risen more during the pandemic, but fewer Americans have benefited. During the last housing boom, house price increases were also staggering, but limited to fewer parts of the country. And that fairness largely disappeared in the kind of failure that economists say will be far less likely this time around. A better analogy, suggested Mr. Keys, might be the Oklahoma Territory land rush in 1889, or the Los Angeles oil boom in the 1920s, events that abruptly changed who owned land and how much it was worth.

The $6 trillion figure estimated by the Federal Reserve does not include all shares of rental housing. So it is an underestimation of the wealth that has recently been piling up on the housing market.

Hard-to-predict events, such as a painful recession, can of course still reclaim some of this total. And this wealth is not the same as having money in a bank account. To use it, households must sell a home or extract its value through a tool such as an equity loan, and that is not without risk. But there is evidence showing that homeowners actually have home equity – to send their kids to college, start a business, invest further in housing and build even more wealth.

“There is a rosy picture and a less rosy picture,” said Emily Wiemers, an economist at Syracuse University who has studied how families use their own funds to pay for higher education. “The flip side is quite disturbing. There is a group of children whose parents have no home and thus have not seen this increase in wealth, as well as whose parents may have seen a decrease in income.”

Understanding inflation in the US

The cumulative effects are profound and diverse: this period of increasing equality will allow some families to create intergenerational wealth for the first time. It will force other families to postpone home ownership for years.

It will increase inequality as profits go disproportionately to baby boomers (at the expense of millennials who will one day buy their homes) and to white households, who have home ownership rates 30 percentage points higher than black households. But black households who own a home will benefit mainly because black household wealth is predominantly in the form of housing.

“I don’t think there’s a viable alternative to homeownership right now” in terms of wealth-building, said Cy Richardson, the senior vice president for programs for the National Urban League, which promotes homeownership among black families. “And it’s an economic disaster for black families who can’t acquire home ownership.”

The highest-income households, which own the most expensive houses, have made the greatest total gains. But because homeownership is so pervasive in America, the poorest fifth of households have also added about $600 million in equity over the past two years. In percentage terms, they have seen the largest increases in prosperity.

Homeowners who remember the 2008 housing crisis may feel nervous about this. But this is a very different housing market, said Mark Zandi, chief economist at Moody’s.

The bubble in the early 2000s was characterized by risky lending and overbuilding. Today home buyers are on much firmer ground with their credit scores, conventional mortgages and pandemic savings. Today there is also a housing shortage nationwide. And that has collided with rising demand from historically low mortgage rates, from families seeking more space during the pandemic, and from remote workers who could relocate to more affordable places. As a result, house prices have risen almost everywhere (making many of those affordable places not so affordable anymore).

Price growth is likely to slow as interest rates rise rapidly, but economists generally do not expect prices to fall. There is simply too much demand for too few homes in America these days. Rising rates will make it more expensive to access equity. But this equity, said Mr. Zandi, “will prove largely sustainable.”

Black Knight, a company that tracks the mortgage market, estimates that the average homeowner with a mortgage has gained $67,000 in “tappable equity” in the past two years. That’s real cash that households can access while still keeping 20 percent of the equity in their homes, as lenders often require.

By that measure, the average mortgagee in the metropolitan area of San Jose, California, has raised $230,000 in two years. In Boise, Idaho, it’s $114,000. In Cleveland it’s $27,000.

“For large swaths of American households, this is great,” said Michael Lovenheim, an economist at Cornell. “And it’s not just for the super-rich, and it’s not just for those who live in the big superstar cities. This is also happening in Ithaca.”

Frequently asked questions about inflation

What is inflation? Inflation is a loss of purchasing power over time, meaning your dollar won’t go as far tomorrow as it did today. It is usually expressed as the annual price change for everyday goods and services such as food, furniture, clothing, transportation, and toys.

Mr. Lovenheim found that families who experienced higher house prices while their children were in high school were more likely to send their children to college. And the kids who went to college went to public flagship universities more often than to community colleges.

He and colleagues also found that households with rising home values were more likely to have children. The work of other researchers has shown that they are also more likely to start new businesses.

“Is this wealth real?” said Mr Lovenheim. “People pretend it’s real.”

The first home that Julio Velezon II was able to buy in Springfield, Virginia, in 2019, measurably changed his life. He and his wife had their first child in that townhome. After that, they were able to buy a larger single-family home in December and keep the first home as a rental home.

If they hadn’t bought in 2019 — before current house prices and current rental inflation — he knows exactly how his life would be different: Not buying a house, he said, would mean not having a son.

“I wouldn’t have felt comfortable having a child when we moved and rented,” said Mr. Velezon, a 35-year-old Air Force technical sergeant. “Renting is such an unknown variable – it’s at the mercy of someone else, to the market.”

Now he imagines that his 18-month-old son could one day live in one of these homes as an adult.

Similar stories are increasingly out of reach for other families who come to First Home Alliance, a housing nonprofit based in Northern Virginia that helped Mr. Velezon. Today, a family making $70,000 a year cannot compete for a three-bedroom home in the area.

“Some of them just have to wait,” says Larry Laws Sr., the president of First Home Alliance (a nonprofit that he started with his own home equity). “We can educate them on the process, make them fully qualified for affordability. But they can’t buy into this area.”

Instead, they wait for their incomes to rise, or for house prices to fall, or for new construction to get underway.

But going forward, Mr. Keys, the Wharton professor, worries that all this housing wealth will only amplify aspects of the U.S. housing market that are fundamentally problematic: that families feel they have few alternatives to build wealth, that housing should serve as both shelter and financial assets, so that homeowners are motivated to protect those assets.

“There’s actually something that’s kind of pernicious about this,” he said. In a sense, millions of people have made trillions of dollars in the past two years doing nothing.

“But it’s worse than that,” he continued. “It’s not that they don’t do anything; it’s that they have aggressively blocked development in so many places.

This wealth was created, he said, precisely because it is so difficult to build houses in America. And that could make it even harder to build more of them.