Officials of the Federal Reserve are planned to release their first series of economic projections this year, in addition to their interest decision, on Wednesday. These predictions offer a new glimpse of the process for the monetary policy at a very uncertain moment for the central bank.

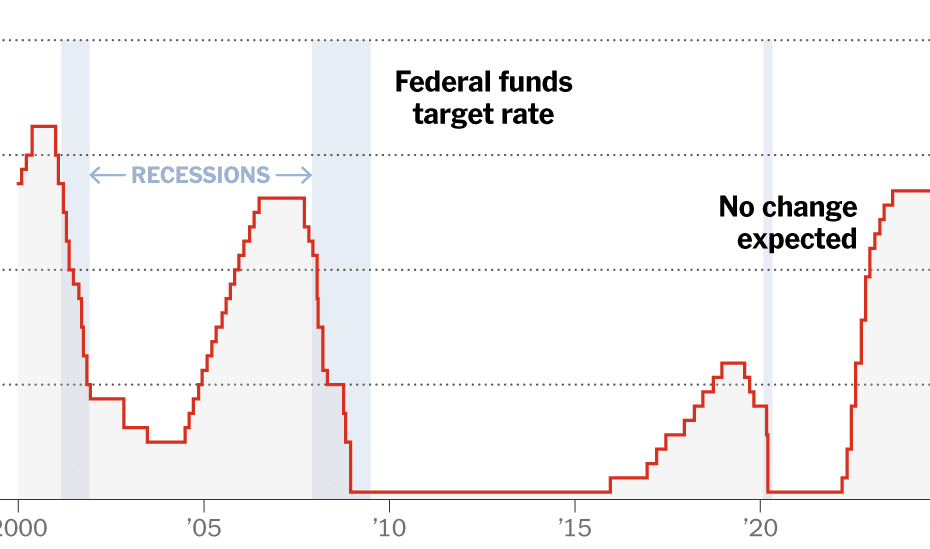

Policy makers paused the reduction in interest in January after reducing the loan costs by one percentage point in the second half of last year. They are expected to be again on Wednesday because they are waiting for more clarity about how far President Trump will push his worldwide trade war and to what extent he will continue with other central aspects of his agenda, including beating government spending and depering migrants.

The big question now is when – and to a certain extent or – the FED can restart this year.

When the FED last released three -month economic projections in December, officials were in two interest rates that would reduce the loan costs by half a percentage point in 2025 by a half a percentage point. But economists now expect Mr Trump's policy to lead to a more intense price pressure and a slower growth, a heavy dynamic for the central bank and one who can ask policymakers to switch back how many spending cuts will continue.

This is what can change and how to interpret those updates.

The pointed plot, decoded

When the Central Bank releases its summary of economic projections every quarter, Fed Watchers focus on one part in particular: the Puntplot.

The Puntplot shows the estimates of FED policy makers for interest rates until 2027 and the longer run. The predictions are represented by dots that have been arranged along a vertical scale – one dot for each of the 19 officials of the central bank.

Economists carefully look at how the dots shift, because that can give a hint about where the policy is going. They fix the most carefully in the middle, or median, dot. This is regularly quoted as the clearest estimate of where the central bank sees the interest over a certain period.

The central bank tries to achieve two things when the policy states: low, stable inflation and a healthy labor market.

When the increased inflation regards care, it increases the interest rates to make borrowing money more expensive, which cools the economy. By removing steam from home and labor markets – as it did between March 2022 and July 2023 – higher rates helped to weaken demand and made it harder for companies to increase prices without losing customers, ultimately weighing up inflation.

With inflation more under control, officials began to lower in September, and started a large reduction of half a percentage point. At the time, the chairman of the Fed, Jerome H. Powell, invoiced it as a movement that would help protect a strong economy, rather than a panic response to unexpected weakness. The Fed reduced interest rates twice as much in 2024, which brought them to the current level from 4.25 percent to 4.5 percent.

Based on the shifting of perceptions about the risks concerning inflation and growth, economists in broad lines expect officials to cut back in one or two quarter points this year.

Are the interest rates still restrictive?

When reading the Puntplot it is important to pay attention to where interest estimates fall with regard to the long -term median projection. That number is sometimes called the “natural” or “neutral” speed. It represents the theoretical dividing line between the monetary policy that has been established to accelerate the economy versus a policy intended to delay it.

The neutral estimate was steadily checked in the past year and in December was 3 percent.

During the last meeting, Mr Powell described rates at their current level as 'meaningfully restrictive', which suggests that the FED sees its policy environments as continuing to weigh on the economy and helps to retrieve inflation. Economists will see if the chair at that point changes his number. If he suggests that rates are no longer so restrictive, this may mean that the FED now sees less capacity to lower the rates with inflation still too high.

Inflation problems are coming up again

The price pressure has decreased considerably since the peak in 2022, but inflation is generally yet to return to the target of 2 percent of the FED. The progress in the direction of that goal has been very bumpy in recent months, and with Mr Trump who apparently commits himself for an aggressive tariff regime, there is more concern about this progress that can be thrown further from the course.

FED officials have moved their estimates for inflation in December strongly higher, while some already started to lay down assumptions about what they could expect from another Trump administration at that time. At the time, the majority expected that the core expenditure of the core of personal consumption – which removes volatile food and energy articles and is the preferred meter of the FED – would float by 2.8 percent by the end of the year. From January it was 2.6 percent.

Policy makers can raise those estimates again on Wednesday, given the scope and scale of Mr Trump's plans so far.

Economists and policymakers agree that rates lead to higher consumer prices, but whether that increase leads to continuous higher inflation is not entirely clear. Much will depend on how extensive the rates are ultimately, how long they are kept in place and ultimately how companies and consumers react.

Is the soft landing in danger?

As many as economists and policymakers are concerned about revival of inflation, they are also concerned about growth, despite the fact that the labor market has been much more resilient than expected despite the rising inflation and increased interest rates.

In December, FED officials expected that the economy would grow by 2.1 percent this year, a moderate pace than 2024 but still a healthy clip. They also expected the unemployment rate to be around 4.3 percent, 0.2 percentage points higher than the level of February.

The estimates with regard to growth are likely to be reduced in the last series of projections, while unemployment predictions can rise as civil servants invoicing Mr Trump to clear the federal workforce and reduce the expenditure.

The feelings of Americans about the economy are already considerably acidified by the fear that all the uncertainty surrounding Mr Trump's trade policy will also lead to companies going to invest the investments and acceptance. Yet most economists do not expect recession, given the strong basis of the economy.