While many people still have Apple (Nasdaq: AAPL) Stock, I think it's time to let it go. The share has been a great artist in recent decade, but all his recent profits are due to investors who offer the share, rather than the actual business performance.

Apple has produced a number of very silly quarters in the last three years and there is no indication of any growth on the horizon. As a result, it is only a matter of time before the market corrects itself and Send Apple to a more reasonable price level.

Apple does not need any introduction. It is one of the most popular technical brands worldwide, but especially in the US, the product ecosystem that it has built is unparalleled and many users.

However, Apple seems to be behind in one of the most important technological varieties to date: artificial intelligence. A large part of Apple's income comes from iPhones, and the AI function, Apple Intelligence, leaves much to be desired compared to its Android competitors. This was clear in the first quarter of a tax year 2025, which ended on December 28, 2024. Apple's Q1 includes the most important holiday area when most iPhones are sold. If the iPhone sales in Q1 is enriched, it is clear that the latest launch was successful. If they remained flat, it is clear that the phone has brought nothing new to the table.

With the help of this measure it is safe to say that Apple has not moved the needle for a while.

Year

iPhone -Income

2024

$ 69.1 billion

2023

$ 69.7 billion

2022

$ 65.8 billion

2021

$ 71.6 billion

2020

$ 65.6 billion

Data source: Apple.

The iPhone income from Apple has really not gone anywhere for a period of five years. This gets even worse when you take inflation into account, because the $ 65.6 billion in iPhone sales during the holiday quarter in 2020 is equal to $ 79.5 billion in 2024 dollars.

So, based on inflation, the iPhone sale has fallen over the past five years. Now that the iPhone sales are 56% of the turnover, this is not a good sign for Apple.

In general, the turnover of Apple year after year increased by 4%, but thanks to efficiency improvements, the profit per share (EPS) increased by 10%. This shows that, although Apple has no growth, management does excellent work to maximize profitability.

However, that type of growth is essentially market average, so the share should act on what the broader market does.

Although Apple's financial performance is essentially market average, its shares are appreciated as those of the next largest growth company.

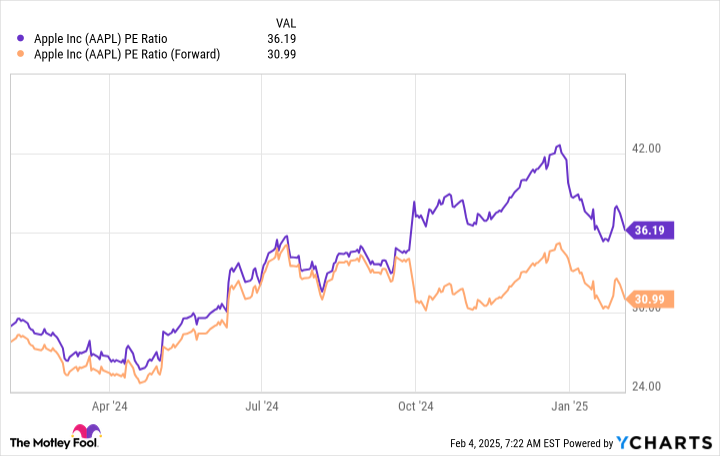

Apple shares acts no less than 36 times behind and 31 times forward income.

AAPL PE -Ratio data by Ycharts. PE = price gain.

Compared to the S&P 500Those 25.5 times deals with a profit and 22.3 times forward income, Apple has a premium of around 40% compared to the market.

Now I will buy the idea that Apple has to govern a premium because of the incredible brand value, but 40% is far too high a premium for only brand value.

There are much more attractive investments than Apple, because several companies act for a cheaper price tag and have a stronger growth than Apple. Here are only a few:

Company

Forward p/e

Last quarter diluted the EPS growth

Nvidia

26.2

111%

Taiwan semiconductor

22.2

54%

Meta platforms

27.6

52%

Salesforce

30.2

35%

Alphabet

22.4

21%

ASML

29.4

30%

Data source: Ycharts.

These are all much more attractive investment options than Apple and represent growth at a reasonable price.

If a final ending point, if you own an S&P 500 index fund, you already have almost 7% of the fund in Apple shares. That is already an important weighting, and further exposure to a company that does not produce spectacular results, is not a sensible investment strategy.

There are far too many other promising companies to waste time with Apple as an individual company. As a result, I think it's time to continue with Apple Stock and to concentrate in more promising areas.

Have you ever had the feeling that you missed the boat to buy the most successful shares? Then you want to hear this.

In rare cases, our expert team of analysts gives one “Double Down” Recommendation for companies that they think is about to pop. If you are worried that you have already missed your chance to invest, this is the best time to buy before it is too late. And the figures speak for themselves:

Nvidia:If you invested $ 1,000 when we doubled in 2009,You would have $ 323,686!**

Apple: If you invested $ 1,000 when we doubled in 2008, You would have $ 44,026!**

Netflix: If you invested $ 1,000 when we doubled in 2004, You would have $ 545,283!**

At the moment we are publishing “Double Down” warnings for three incredible companies, and there may not be a different chance soon.

More information »

*Stock Advisor Return on February 3, 2025

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and Sister of Meta Platforms CEO Mark Zuckerberg, is a member of the Motley Fool's Board of Directors. Suzanne Frey, a director of Alphabet, is a member of the board of directors of the Motley Fool. Keithen Drury has positions in ASML, Alphabet, Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has positions and recommends ASML, Alphabet, Apple, Meta platforms, Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

It's time to sell Apple Stock. This is why. was originally published by the Motley Fool

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.